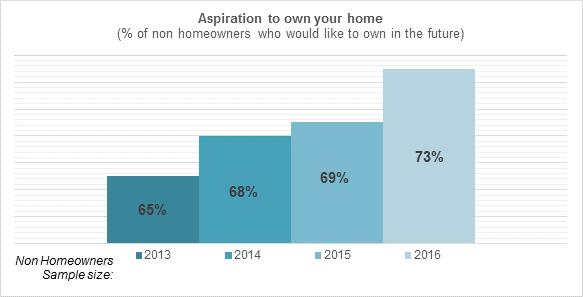

64% of would-be homeowners rent first

Nearly two-thirds (64%) of would-be homeowners in Britain rent a property before picking up the keys to their own place, according to new research.

Data from the report by Clydesdale and Yorkshire Banks underlines the difficulty that many potential buyers are facing in the current market.

Renters’ struggles

Saving up for a deposit is one of the greatest hurdles facing first-time buyers. The survey found that renters are not likely to get assistance from their family, with only 41% saying that this was the case. This was in comparison to 62% living with their parents.

Building up a sufficient deposit is also a challenge to tenants currently living in the rental market, with an average months rent standing at £681.70.

Of those living with their parents before purchasing their own home, 21% said they don’t pay rent. One-third of would-be homeowners said that they put this money towards their deposit instead.

52% said that they pay a fixed amount each month to their family, with 22% contributing towards food and bills.

Stress

In addition, the research found that those currently residing in rental properties find getting a foot on the property ladder more stressful. 28% admitted they were finding the process difficult, in comparison to 16% of those still living with their parents.

Steve Fletcher, head of customer banking networks at Clydesdale and Yorkshire Banks, said, ‘buying a first home is one of life’s most significant financial milestones and the banks can work with the individual needs and circumstances of potential first time buyers to help make their dreams of becoming a homeowner a reality.’[1]

64% of would-be homeowners rent first

Cover

Additional research conducted by Royal London indicates that nearly five million renters in Britain have no plan in place to cover their rental payments, should they become too ill to work.

This alarming figure comes despite 27% of renters in work saying they were aware of someone who had struggled in a similar situation. 34% admitted they didn’t know how long they could pay their rent for should they be unable to continue in their employment

60% said that they could only continue paying their rent for three months or less.

Solutions

In terms of solutions, 53% said their first move would be to apply for state benefits, while 47% would cut their expenses and 39% would use their savings.

Just 7% of renters in employment said that they had consulted a financial advisor.

Debbie Kennedy, head of protection for Royal London Intermediary, noted, ‘renters who assume that housing benefit will be there when they need it could find the reality is very different. A series of cuts to housing benefit means that more people would not get their rent paid in full if their income fell unexpectedly.’[1]

‘It would be bad enough to be taken ill without the added anxiety of getting behind with the rent and facing possible eviction. Income protection may be more affordable than people realise and can provide a financial safety net and enable people to focus on getting better,’ Kennedy added.[1]

[1] http://www.propertywire.com/news/europe/uk-property-market-buyers-2016052411948.html