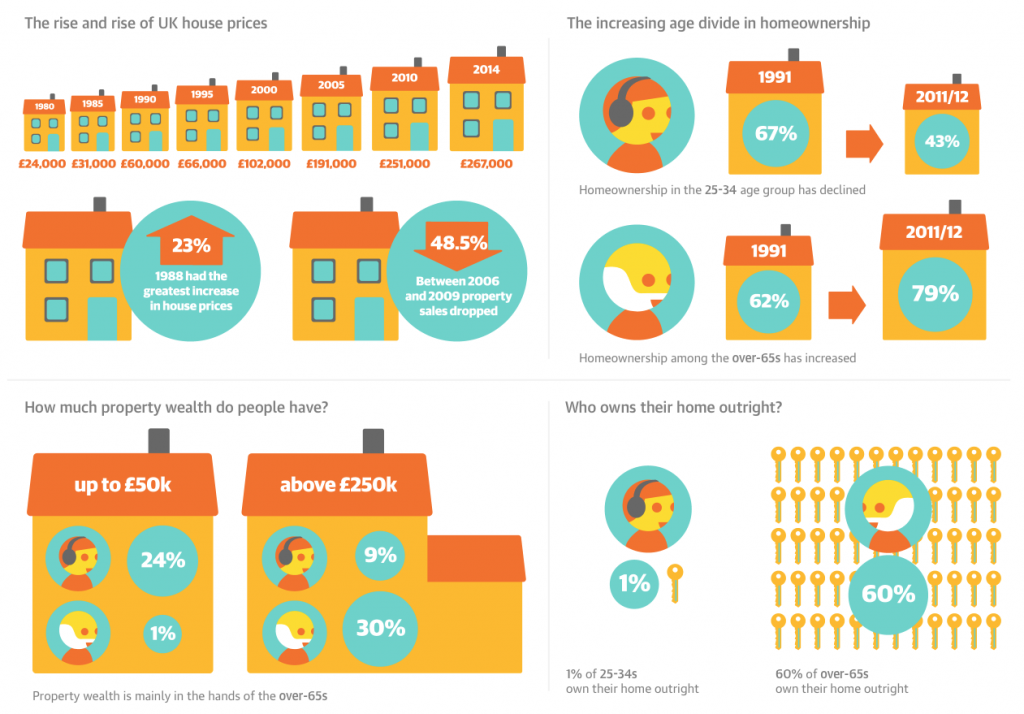

First time buyer house prices increase in June

New research has indicated that the average price of a first-time buyer home rose by over £4,150 in the last month.

A report from Haart shows that homes grew in value by £138 every day in the past month and by £12,000 over the last year.[1]

Rises

Data compiled by Haart shows that the average UK property price is now £216,951. This represents a 6.1% rise over the year and 2.6% on the month and is a new high, continuing the upward spiral of prices since November.[1]

For first-time buyers, the average price of a home saw a larger increase of 7.5%. Starter homes also grew in value by 2.6% in June to stand at £166,393. The total number of first-time buyers however was down 13.6% annually.[1]

Additionally, first-time buyers made up 42.7% of all mortgages taken out in June, down from the 44.4% a year earlier. This data suggests buyers are still finding it difficult to get a substantial foothold in the market. What’s more, the average first-time buyer mortgage was up 3% in June and 8.7% in the year.[1]

New buyers registering increased slightly by 0.5% but supply was found to be lacking, down by 0.7% monthly and by a substantial 13.9% annually.[1]

First time buyer house prices increase in June

Changing reality

Paul Smith, CEO of Haart acknowledged, ‘first-time buyer house prices climbed £4,150 in a single month or £138 every day in June. A potential first-time buyer on an average salary of £27,000 must be prepared to spend 42% of their take home salary on mortgage repayments, showing the traditional rule of spending no more than 30% of income on housing is no longer reality for many.’[1]

Smith said that, ‘as a result, we’ve seen a knock-on effect on first-time buyer registrations which are down 13.6% annually. The only solution to this is to unlock the market and free up supply.’ He went on to suggest that, ‘efficient use of space is a must and we need to dispel fears that downsizing indicates older homes have lost their zest for life. Movement in the upper echelons of the market will free up stock at all levels and put the brakes slightly on property price growth.’[1]

‘There are currently 11 buyers chasing every new property to come onto the market in the UK, and in London the figure is nearly double at 20:1. However, the Government’s recent announcement in the emergency Budget that the inheritance tax threshold is to be raised to £1million and that an ‘inheritance tax credit’ will be implemented, should encourage those with larger, more expensive homes to downsize. This should have a trickle-down effect and boost the supply of starter homes at the lower end of the market, helping first-time buyers,’ Smith concluded. [1]

[1] http://www.propertyreporter.co.uk/property/ftb-house-prices-increase-by-4150-in-june.html